Olemedia/E+ via Getty Images

The biggest fear in investing in Qualcomm (NASDAQ:QCOM) was another lawsuit from Apple (AAPL) removing the tech giant as a customer again. After all, Apple bought the modem division from Intel (INTC) in order to build a new 5G modem for the iPhone to replace supplies from Qualcomm. My investment thesis was ultra bullish on the stock, including this likely outcome, but the news of Apple failing to produce a competitive 5G modem is a very positive development for Qualcomm.

Apple Impact

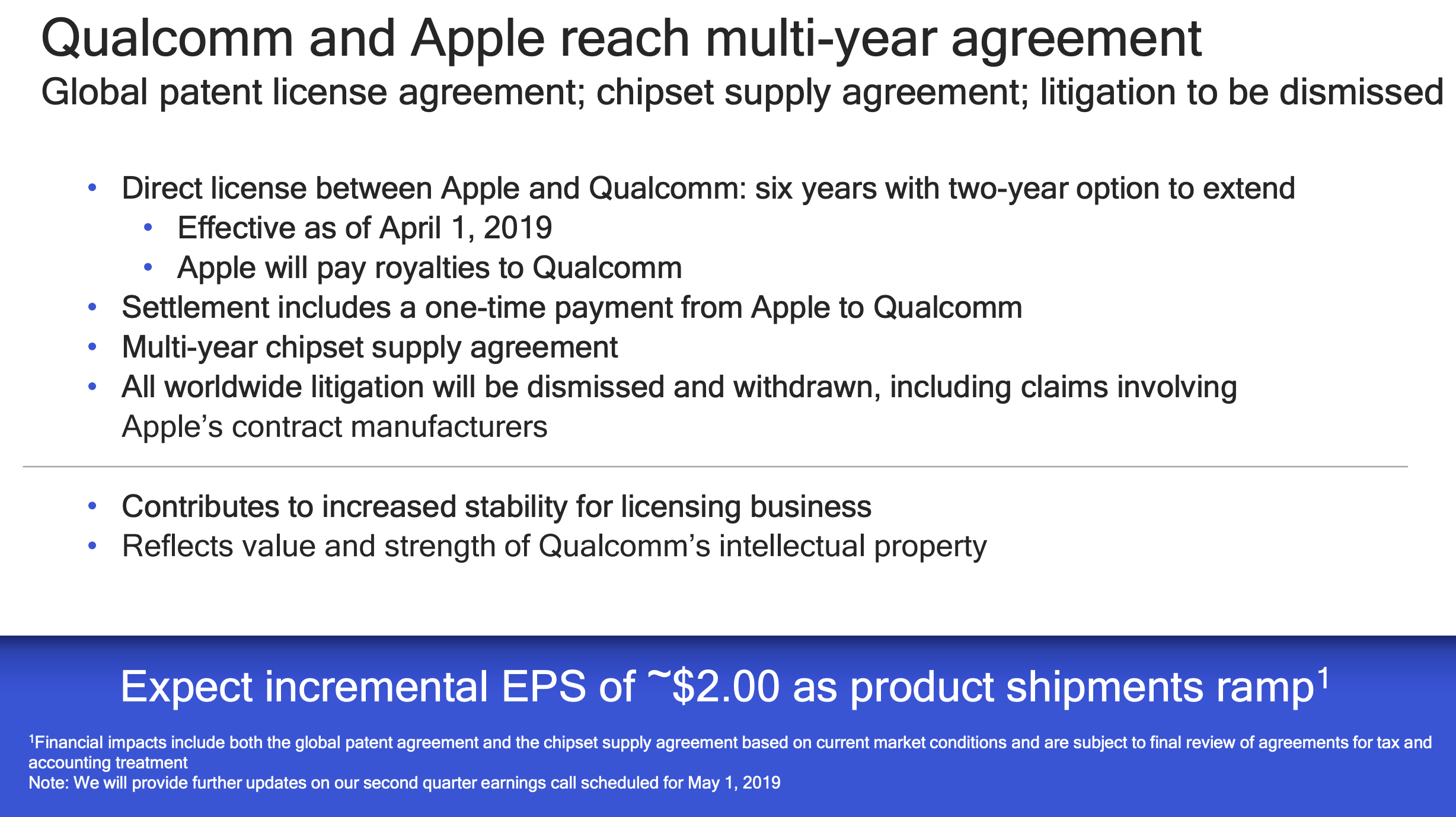

One only needs to go back to the agreement between Qualcomm and Apple to understand the future impact of losing Apple as a customer. At the time, back in 2019, Qualcomm forecasts a $2 EPS boost from the agreement with Apple after a lengthy period of lawsuits.

Source: Qualcomm presentation

A key here is that the $2 EPS boost consists of licensing revenues and modem chip sales. The vast majority of the EPS boost comes from the resolution of the licensing agreement, which wouldn’t disappear on Apple using internally developed modems for the iPhone. The license deal was for 6+ effective April 1, 2019 while the chipset deal was only a multi-year agreement.

Apple developed new CPU chips to replace Intel chips for Macs, but one has to wonder why Apple has even bothered with developing modems. Part of the agreement to obtain modem supplies from Qualcomm was an agreement about the key patents which required Apple to pay ongoing license fees. Whether or not Apple develops internal modems, the tech giant has to pay the license fees due to Qualcomm developing the key technologies necessary to produce 5G speeds.

Apple Problems

The ironic part is that Intel failed to deliver competitive 5G modem chips, so the company exited the business and sold the unit to Apple for $1 billion. Qualcomm had already forecasted that Apple would use internal modems on up to 80% of iPhones in 2023 or the equivalent to FY24.

Influential Apple analyst Ming-Chi Kuo tweeted that the tech giant has failed to produce a 5G modem chip. The development leaves Qualcomm as the sole supplier of modems for the iPhone into 2024, at least.

The big question is whether Apple is able to ever produce a 5G modem capable of matching the Snapdragon produced by Qualcomm. At the earliest, Apple would have a modem for the iPhone launch in 2024 or essentially FY25.

In a couple of years, Qualcomm should see the Automotive business start to produce material revenues. The wireless giant has an order book of $16 billion, and EVs and AVs should start hitting the market in full force in the 2024 to 2026 timeframe. The company has already forecast Automotive revenues reaching $3.5 billion annually in a few years.

Considering the only risk to Qualcomm is the chip revenues originally estimated as $0.50 of the $2+ EPS target from the Apple business, the Automotive business can easily replace any lost earnings from the tech giant. The Automotive sector offers far more content than a smartphone, and Qualcomm also expects to see far more upside in the IoT segment.

Remember, the stock is cheap and analysts should have already factored in the loss of the majority of the Apple modem business into financials. The stock trades at just 9x FY23 EPS targets, and the company might not even lose any business from Apple for FY24.

The Automotive and IoT segments provide major growth opportunities for the years ahead. The hope is that Qualcomm is no longer reliant on Apple as a driver of earnings. The company should continue to obtain the large royalty fees from iPhone sales, but the modem chip sales will soon become a side note for the business.

Takeaway

The key investor takeaway is that Qualcomm is now priced for a major global recession and losing Apple as a customer. Neither might happen, while the wireless chip giant has plenty of growth opportunities ahead in areas such as Automotive and IoT.

Investors should continue to use the weakness to load up on a leader in the semiconductor space forecast to grow for years ahead.

{kind=link}