masterSergeant

Thesis

Readers familiar with my writing know that I am a long-term bull of Apple (NASDAQ:AAPL). And lately, with large market volatility, the market ratings of AAPL have shown large variances. Take the articles published on Seeking Alpha as an example. In August 2022, the ratings had been pretty much dominated by a bullish thesis. But for the 10 most recent articles as of this writing, 2 recommended “Buy”, 4 recommended “Hold”, 2 recommended “Sell”, 1 recommended “Strong Sell”, and the last one is a portfolio strategy article involving AAPL without a rating.

I am a steadfast AAPL bull. And my favorite Charles Munger quote is not to comment on a topic until I can argue against myself better than the people on the other side. Following this wisdom, the focus here is to address the risks facing AAPL, especially those that are not often discussed by other SA authors. To recap, other SA bears have eloquently analyzed risks such as valuation risks, growth potentials, iPhone 14 sales, et al. Before I go any further, let me emphasize that the point of this article is not to prove the bears to be wrong. On the opposite, their concerns are 100% valid. I am here to hear them out and provide my thoughts so both bulls and bears can all make informed decisions.

I won’t add on to these above risks anymore, as they have been discussed by other SA authors thoroughly already. And my view on these issues is also detailed in my earlier articles. I do not see too many valuation risks given its profitability. And from a long-term business owner’s point of view, I do not need too much growth from a perpetual compounder like AAPL to achieve double-digit returns.

In a word, my view is that the main risks associated with AAPL do not come from valuation risks, profitability, or the success or failure of any one of its products like the iPhone 14. In my mind, the biggest one is its large exposure to China and the ongoing structural risks associated with China. From the data that I can gather, AAPL products are still hugely popular in China and the China market has become increasingly more important for AAPL. But like many things in life, too much of a good thing becomes a bad thing at a point. And the thesis of this article is to show that there are earlier warning signs for the arrival of this point. These risks include the possibilities of new lockdowns, China-US trade tension, China’s role in the currency market, and also the possibility of a recession in the overall Chinese economy.

We will analyze these risks in more detail next. And you will see why I am concerned. To me, any of them could fundamentally change the Apple thesis if any of them materializes. And finally, based on the analysis, I will provide some hedging ideas at the end.

iPhone 14’s popularity in China

I am not too concerned about the popularity of its products for two reasons. First, AAPL has built up such a strong ecosystem already that the failure of a particular given product is both inevitable AND also noise to me. Second, its products are still hugely popular. Take its latest iPhone 14 as an example. Since its release on the 8th of September, the popularity of the iPhone 14 series has continued to rise as many of its predecessors. From data on JD.com (JD), the number of reservations for the iPhone 14 series has already exceeded one million in a week in China. In physical Apple stores, swarms of AAPL fans are still queuing up for the new iPhone 14. Furthermore, the iPhone 14 and other iPhones are at the top price tier of the Chinese smartphone market, enjoying a disproportionate profit margin.

While AAPL investors of course should be happy about the continued popularity of iPhone 14, and AAPL products, we need to be aware of the ongoing risks associated with China, as discussed next.

China’s larger role and uncertainty

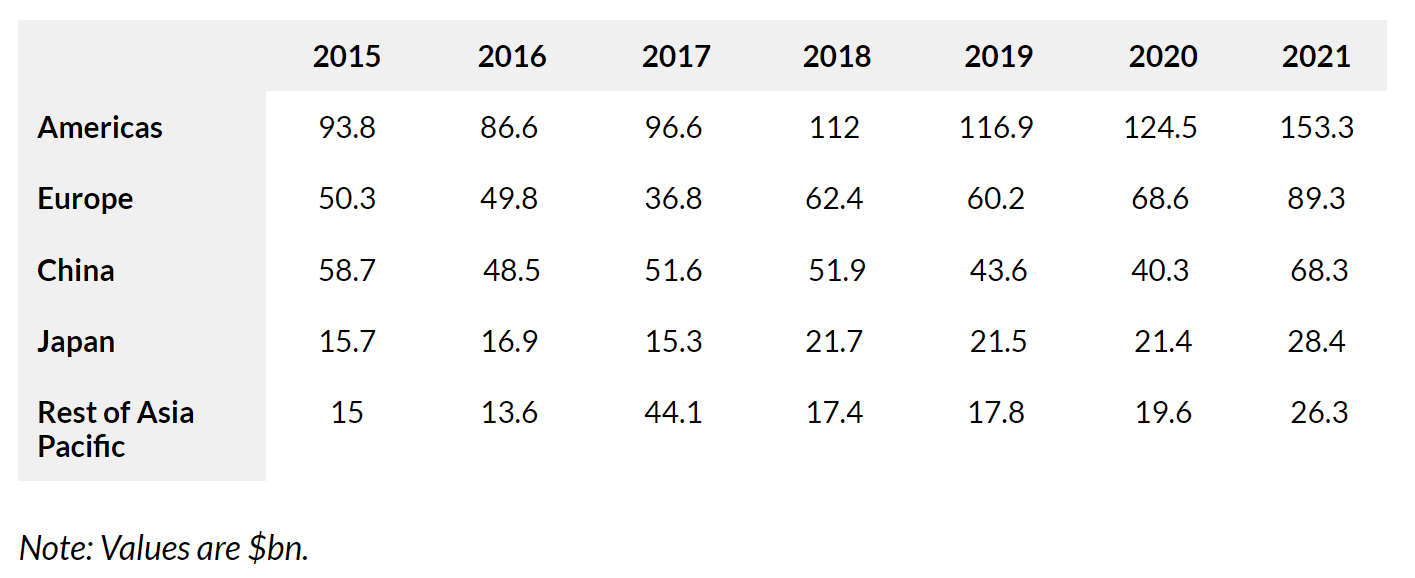

China is not only important for iPhones, but also for other AAPL products as well. The following chart shows Apple sales by region from 2015. As seen, its sales in China have been steadily growing over the years, from $58.7 B in 2015 to $68.3 B in 2021. In terms of its sales composition, the Americas are currently responsible for 40% percent of all revenue (hence a relative minority). And the majority 60% of its revenues are generated overseas with China being the 3rd most important market, only after Europe.

Source: businessofapps.com

Such large exposure creates a key risk going forward, not only due to the size of the exposure but also due to the unevenly distributed growth potential as argued in my earlier article below. The growth potential is very uncertain in China due to both lingering lockdowns earlier this year and also the possibilities of new lockdowns such as what has transpired in Chengdu recently. Also, the pandemic, when combined with other issues in China, could trigger a full scales recession in China (or even globally). And AAPL, as a premium brand, will suffer immensely.

AAPL’s growth of 9% in the past quarter was unevenly distributed geographically though. North America grew about 19%, while Europe and greater China’s growth are more muted. And at the same time, the greater China market is the third-largest market for Apple, a close third after the Europe market. Its total sales in the past six months are $44 billion, not too far behind the Europe market, which raked in $53 billion in the past 6 months. Looking forward, the ongoing COVID shutdowns in China, especially in a key port city like Shanghai, could negatively impact iPhone deliveries and sales in the near term. As commented by CEO Tim Cook (the emphasis were added by me):

“I also want to speak to the unpredictable nature of the pandemic. We are excited to be welcoming employees back to the offices in the US and Europe. At the same time, we are monitoring COVID-related disruptions in China.”

AAPL Q3 earnings report

Competition and geopolitical risks

Besides the above risks associated with the pandemic and recession, AAPL also faces fierce competition from local brands. And to make things even worse, such competition is inseparable from the ongoing geopolitical tension between the US and China.

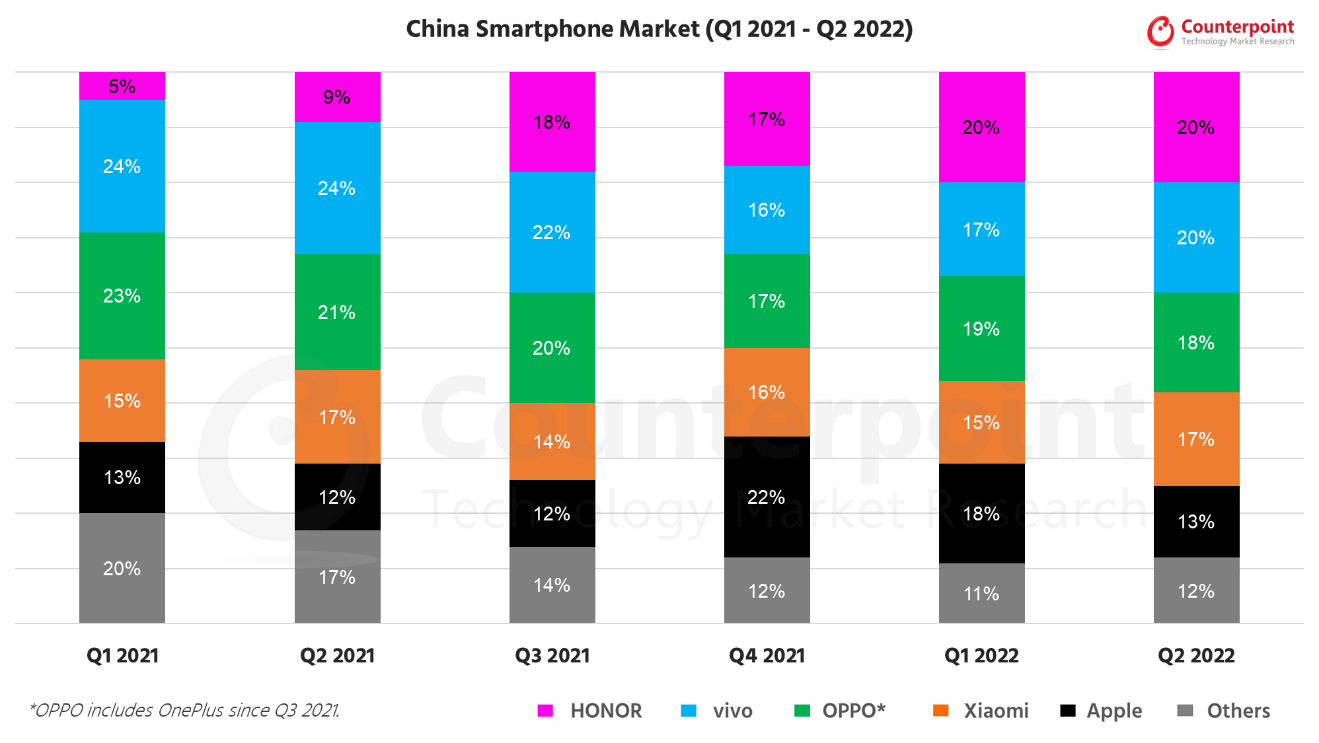

For example, when Huawei was placed on a trade blacklist in 2019, there had been a strong voice in China to boycott Apple products too. And as you can see from the chart below, iPhone’s market share in China has been declining since its peak in 2021 Q4, when it grabbed 22% of the China smartphone market. In Q2 2022, iPhone’s market share declined to 13%, a whole 900 basis point decline from the peak. In the meantime, local brands such as Huawei Honor and Xiaomi Vivo have been grabbing top market shares quite steadily. The silver lining here is that despite the lower market shares, AAPL has been raking the most revenue because of the premium pricing. For the first half of the year, Apple’s sales exceeded RMB47 billion, accounting for about 55% of the total China smartphone sales. Xiaomi ranks second, with sales of only about RMB13 billion.

Because the China market is a key market for AAPL, such competition and geopolitical risks far outweigh other risks (like valuation and iPhone 14 sales) in my mind. These risks could have unpredictable rippling and lingering effects.

Source: counterpointresearch.com

Other risks and final thoughts

Besides the above risks, AAPL also faces strong currency headwinds as a global business. Its FY2022 Q3 guidance assumed a 6% impact from foreign exchange rates in 2022. However, since the FYQ3 earning report, the persisting inflation may cause the Fed to hike up rates further and cause further dollar strengthening and causing even stronger currency headwinds than expected. Two other factors further complicate the currency risks: A) the ongoing trade tension between China and the US, and B) the fact that China is still the largest foreign holder of the dollar.

To close, the purpose of this article is to argue against my own bull thesis on AAPL. Besides the often-mentioned bearish arguments (such as valuation and muted growth), I also see other risks associated with AAPL such as competition from local China brands, currency headwinds, and global supply chain disruptions. But overall, I see the risks associated with its large China exposure as the most important antithesis. In particular, key risks include new lockdowns in China due to the COVID resurgence and the escalation of China-US trade tension. Competition and growth in the China market are inseparable from these geopolitical risks. And if any of them materializes, it could change the Apple thesis more fundamentally than other often-discussed factors such as valuation risks and softened iPhone 14 sales.

Finally, a few hedging ideas. My view is that you don’t have to worry about it unless you A) agree with the above analysis, and B) hold too many AAPL shares or are too exposed to China in addition to AAPL. If either A or B does not apply to you (like in my case), it’s fine to just hold on. However, in case you are concerned, you could of course reduce your AAPL exposure or other China exposure (the simplest and more direct way). Or for more sophisticated investors, to hedge these “China” risks, you essentially need some sort of “China put” or “Currency Put”. Buying an option or ETF that responds sensitively to AAPL’s China exposure could maximize the use of capital efficiently. For example, a put option on Taiwan Semiconductor, with AAPL being its largest client and its stock prices highly sensitive to the development of the China-U.S. tension, could be one ideal. The Direxion Daily FTSE China Bear 3x Shares (YANG) could be another hedging idea.

{kind=link}